AI-Driven Equity Alpha: Media Sentiment Models for Tech & Energy Equities

Discover how machine learning on 1.1M+ daily news articles turns global media sentiment into predictive trading signals for Nasdaq 100 Technology stocks and US Energy sector equities. Backtested by AltHub on its QuantLab platform over a 3-year out-of-sample period (2023–2025), the long-only portfolios delivered +5.7% alpha on Nasdaq 100 Tech and an exceptional +29.9% alpha on US Energy versus the S&P 500 Energy benchmark — both with beta below 1 and Sharpe ratios above 1.3. Includes full performance results, ML model design, portfolio construction rules, and transaction-cost-adjusted returns.

Get the White Paper

About this White Paper

From narrative to alpha — before the tape catches up.

Markets don't price information instantly. Stories, sanctions, supply disruptions, drilling disclosures and regulatory shifts all flow through the media before they are reflected in equity prices. This paper shows how 1.1M+ daily articles across 220,000+ domains and 12 languages were aggregated through a three-tier pipeline — article → scenario → company — into a clean, ticker-mapped daily time series that integrates directly into existing quantitative frameworks.

See the data in action — across two distinct universes.

Backtested on AltHub's QuantLab using 7 years of training data (2015–2022) and a rigorous 3-year out-of-sample period (2023–2025), the long-only portfolios delivered total returns of 147% on Nasdaq 100 Tech (vs. 126% benchmark) and 152.4% on US Energy (vs. just 7% for the S&P 500 Energy). Both strategies maintained beta below 1 (0.89 / 0.75), confirming outperformance with lower-than-benchmark market sensitivity. Full transaction-cost scenarios at 1, 2, and 3 bps are included.

Sentiment alpha isn't only a tech story.

The standout finding is the Energy sector: a universe traditionally modelled through commodity prices, production data, and macro variables proved equally — if not more — receptive to media sentiment signals than high-momentum tech. The paper details why narrative-driven sectors deliver the largest sentiment alpha, and how a fully replicated, point-in-time investment universe eliminates look-ahead and survivorship bias.

Who it's for:

Quantitative funds, asset managers, portfolio managers, and risk officers building or augmenting equity strategies with alternative data — particularly those seeking low-correlation alpha, sector diversification signals, and ML-ready, ticker-mapped feature sets that plug directly into existing factor models, risk systems, or standalone signal pipelines.

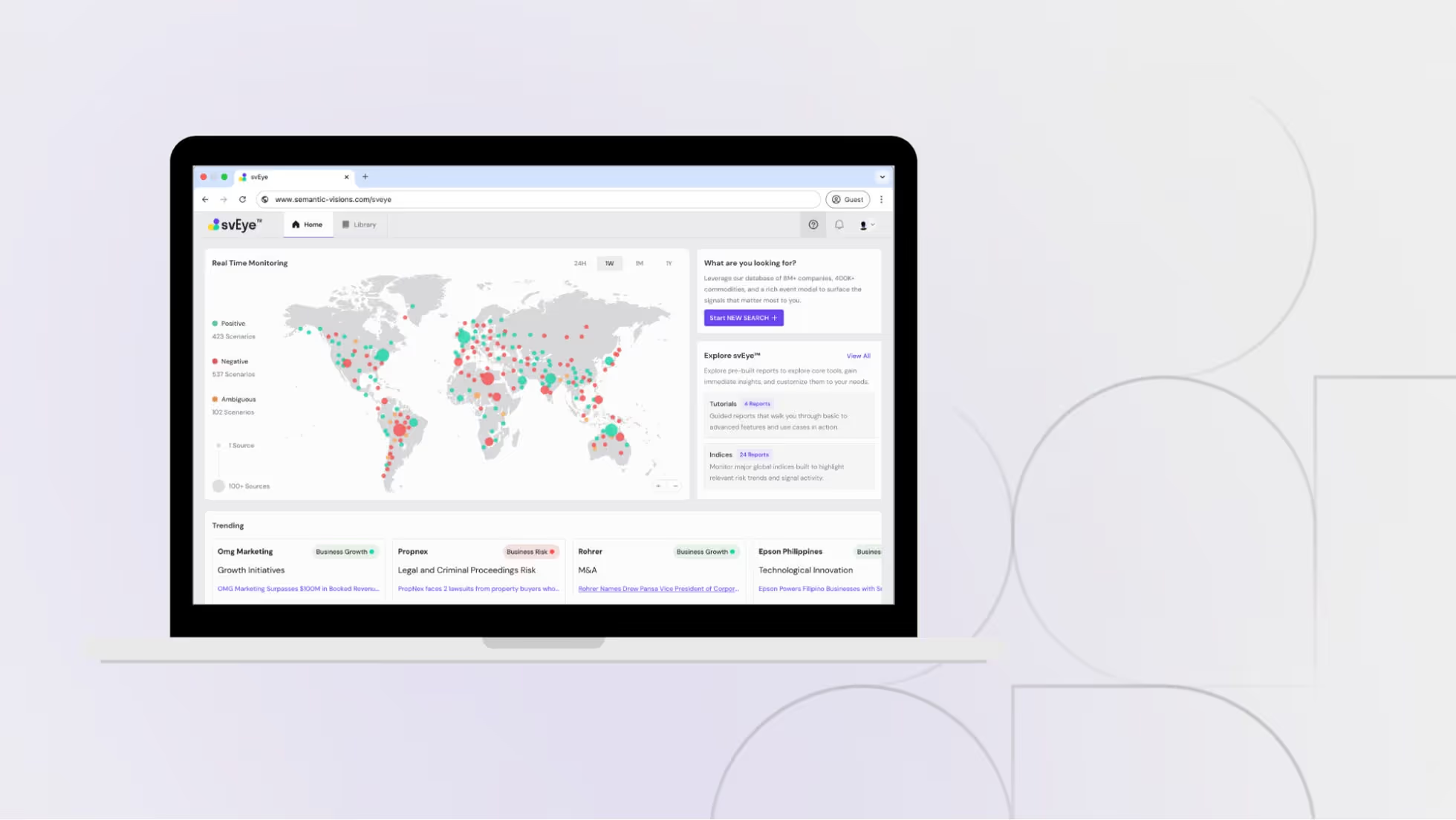

Explore Real-Time Risk Detection in svEye™

See how dynamic event monitoring works in practice. Track supplier and partner risks across jurisdictions, industries, and ownership networks — all in one dashboard.

Map Your Competiton

or Monitor Your Supply Chain

Contact us to get a customized competitive analysis tailored to your industry and specific business needs or discover other tiers of your supply chain. Let us help you stay ahead in the market.